Peak US interest rates in as markets eye cuts in early 2024

Headlines

* Fall in US core CPI slashes odd of Fed rate hikes, rate cuts could come in March

* US shutdown risk drops as more Democrats back GOP Speaker’s plan

* US 10-year Treasury yield tumbles below 4.50%, USD plunges 1.5%, stocks surge

* GBP, EUR hit two-month highs versus the dollar, UK CPI in focus

FX: USD eventually slumped 1.5% after the softer than expected CPI data. All four main measures missed estimates to the downside by one tenth. (Headline y/y and m/m at 3.2% and 0%, core y/y and m/m at 4.0% and 0.2%.) Yields turned sharply lower dragging the dollar down with it. It was the biggest drops vs EUR and GBP since November 2022. The Fed’s policy tightening is seen as done. The issue is now about conveying an ‘on hold’ message. There is now currently a one in three chance of a 25bps rate cut in March and a coin toss in May. The 100-day SMA is at 104.15 and 200-day SMA at 103.60.

EUR rose sharply, gaining 1.82%. The late August highs are at 1.0939/45. The German ZEW survey expectations came in better than expected. Investors appear to be ore positive as inflation eases and the ECB rate cycle peaks.

GBP was the second best performing major currency. Firmer jobs data with payrolls rising and the jobless rate unchanged suggested a market that isn’t loosening. But wage growth did show mild signs of slowing though it is remains elevated.

USD/JPY backed off recent highs as the dollar got sold and Treasury yields plunged. This broke a six-day win streak and provides relief for Japan’s MoF. The 50-day SMA sits at 149.30.

AUD outperformed along with NZD as high beta currencies were bought up. The aussie closed just above the 100-day SMA at 0.6490. But below a major Fib level (38.2%) of July drop at 0.6510.

Stocks: US equities were propelled higher as bond yields fell. The benchmark S&P 500 added 1.91% to settle at 4495. This was its best day since April. The rebound from the late October low just over two weeks ago is 9.55%. The tech-laden Nasdaq finished 2.13% higher at 15,812. US tech stocks hit an all-time high with the “Magnificent Seven” adding more than $200bn to their market cap. They are now roughly 29.15 of the total market cap of the index. The Dow settled 1.43% higher at 34,827. Real estate stocks soared with the sector jumping over 5%, its biggest one-day percentage move since last November. Tesla added over 6% on reports it may produce a cheaper EV in Germany. Nvidia rose to its first record close since August. It has now rallied nearly 22% in a 10-day win streak.

Asian futures are in the green with the Nikkei 225 set to rise above 33,000. APAC stocks traded mixed on Tuesday with gains capped as markets awaited the US CPI data.

Gold rebounded strongly off the 200-day SMA at $1935 and a fib level (38.2%) of the October rally at $1933. Bugs will eye $2000 now if Treasury yields move lower and the Fed’s tightening cycle is finished.

Day Ahead – UK CPI, US Retail Sales, China Data

A busy day of data ahead. First up is the monthly China data dump with retail sales expected to be boosted by the first post-pandemic Golden Week. But the other main data, including fixed asset investments and industrial output are forecast to remain unchanged. The reports will be used to measure China’s ongoing subdued recovery. The latest inflation numbers and manufacturing PMI paint a fragile picture.

UK CPI is likely to fall sharply. The headline is predicted to slide to 4.9% from 6.7% due to base effects and the surge in utility prices from last year dropping out. The core is expected to decline to 5.8% from 6.1%. The all-important services inflation, a gauge the MPC follow closely, is seen ticking one-tenth higher to 6.9%, still lower than the MPC’s 7% forecast.

Finally, US retail sales will be followed to see how much impact higher rates are impacting the US consumer. Bank surveys suggest that household balance sheets are still relatively healthy. The restart of the repayment of student loans is ongoing.

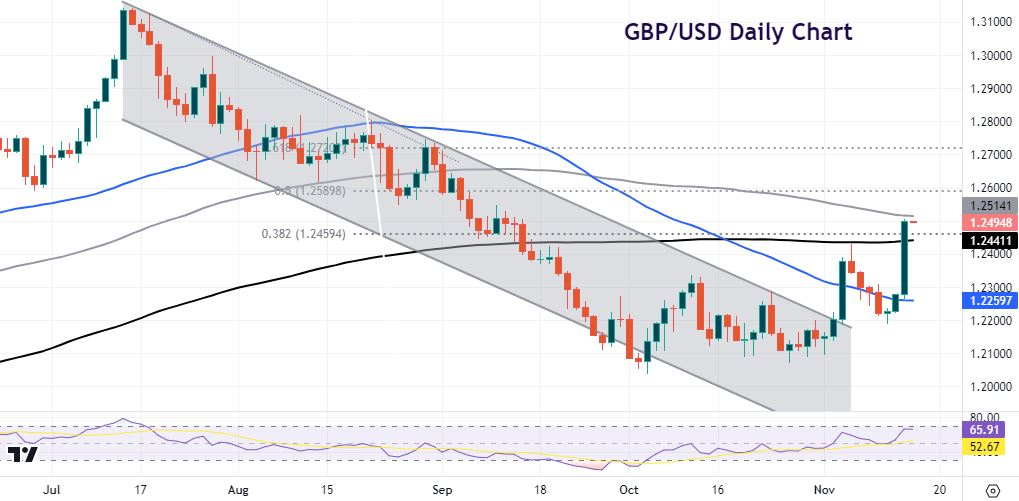

Chart of the Day – GBP/USD breaks higher

Yesterday’s wage data was still inconsistent with the Bank of England’s 2% target. But the trend is hopefully down from here and the same can be said of CPI. A print similar to the US report yesterday may slow the surge higher in cable. But markets reckon the Fed’s work is definitely now finished, while the BoE may still keep rates higher for longer as persistent price pressures remain evident. The 200-day SMA is at 1.2441. The 38.2% Fib level of the July drop sits at 1.2459. Above is the 100-day SMA at 1.2514 and the halfway mark of the July decline at 1.2589.